The recent uptrend in real estate prices has put a lot of people in the good position of having substantial capital gain in their primary residence. It is critical for anyone in this sweet spot to understand their options as the IRS is offering some great tax benefits when selling your primary residence at a gain.

The general rule is that if you have sold your main residence at a gain the first 250K in profit are not taxable, 500K if married filing jointly. In order however to make sure you qualify you need to satisfy all the requirements listed below:

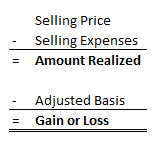

In order to figure your gain of the house you need to follow the following formula:

If you don’t however meet the criteria listed above you can still get a partial exemption if you sold the home because of work-related move, health or unforeseeable event.

You can read the full IRS publication here:

Sources Used:

https://www.irs.gov/publications/p523

Small business owners often struggle with the decision regarding which entity form to use for…

What Is Accounting? Accounting is “the art of recording, classifying, and summarizing in a significant…

Hiring an accountant to look after your business finances is a very smart move. Here…

Tax consultants, also know as tax advisors, are experts in tax law, planning and compliance.…

Why do we feel much better about having our savings in a bank than we…

LIFE INSURANCE TERMS AND DEFINITIONS: insurance - Insurance is a means of protection from…

{kind=link}