This article is a summary of a presentation prepared by Viktor Vasilev, CFA, EA on the topic of how the Tax Cuts and Jobs Act of 2017 affects individual and corporate income taxation.

You can download a PDF version of the presentation here: Tax Cuts and Jobs Act

If you are reading this, you may be feeling a little bit frustrated, as you want to know what changes the Tax Cuts and Jobs Act of 2017 brings to the table. This article aims to help you understand the new tax legislation and how the new tax rules work.

Just before Christmas 2017, President Trump signed the Tax Cuts and Jobs Act into law. This Act is the most drastic update to U.S. tax code in more than 30 years (since Reagan’s Tax reform in 1986). The reforms will lower taxes on individuals and businesses and will simplify tax paying for many Americans.

Main Tax Forms

- 1040 – Â main federal individual income tax form – Form 1040 is used by U.S. taxpayers to file an annual income tax return.

- Schedule A for Itemized Deductions – Â Schedule A (Form 1040) is used to figure your itemized deductions. If you itemize, you can deduct a part of your medical and dental expenses and unreimbursed employee business expenses, and amounts you paid for certain taxes, interest, contributions, and other expenses. You can also deduct certain casualty and theft losses.

- Schedule E for Rental Income – Â Â Schedule E (Form 1040) is used to report income or loss from rental real estate, royalties, partnerships, S corporations, estates, trusts, and residual interests in REMICs.

- Schedule D for Capital Gains – The new thing here is that the election to rollover gain from an empowerment zone is no longer available.

- Mass Form 1 – Mass Income Tax Form

- 1120 Corporate Federal Income Tax Forms – Domestic corporations use this form to: report their income, gains, losses, deductions, credits and to figure their income tax liability.

Definitions

- Adjusted Gross Income –Ðdjusted gross income (AGI) is an individual’s total gross income minus specific deductions.

- Taxable Income – Taxable income refers to the base upon which an income tax system imposes tax.

- Exemptions-. Most taxpayers are entitled to an exemption on their tax return that reduces your tax bill in the same way a deduction does. Federal and state governments frequently exempt organizations from income tax entirely when it serves the public, such as with charities and religious organizations.

- Deductions – Tax deduction is a reduction of income that is able to be taxed and is commonly a result of expenses, particularly those incurred to produce additional income.

- Tax Liability – Your tax liability is the total amount of tax on your income. In addition to income tax, your tax liability can include self-employment tax, household employment tax, and tax penalties such as the 10% early distribution penalty for IRAs.

- Tax Withheld – If you are an employee, your employer probably withholds income tax from your pay. Tax may also be withheld from certain other income — including pensions, bonuses, commissions, and gambling winnings. In each case, the amount withheld is paid to the IRS in your name.

- Tax Refund – A tax refund is the difference between taxes paid and taxes owed. Each year a taxpayer submits a tax return that calculates his or her federal income taxes owed.

Below you will find some of the key points, included in the Tax Cuts & Jobs Act of 2017.

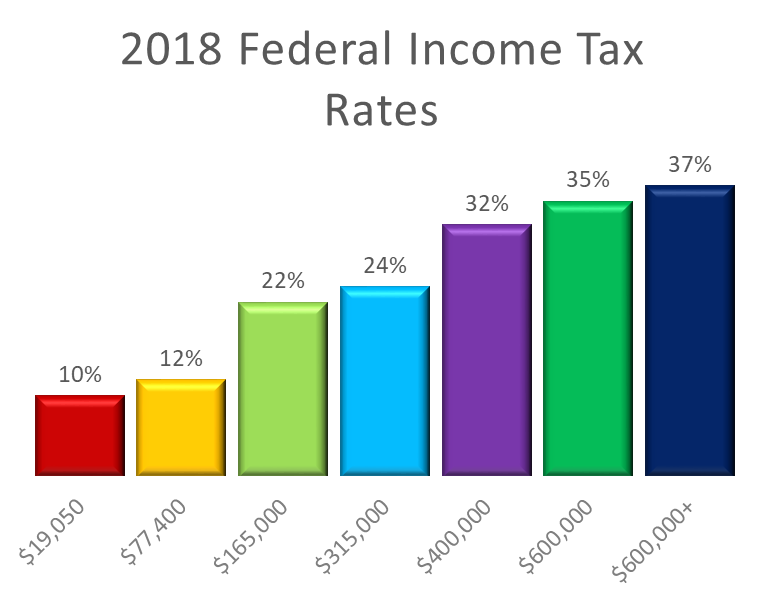

Tax Rates and Effects (MFJ)

In 2018, the income limits for all tax brackets and all filers will be adjusted for inflation. The top marginal income tax rate of 37 percent will hit taxpayers with taxable income of $500,000 and higher for single filers and $600,000 and higher for married couples filing jointly. Tax savings by income level (2018 vs 2017) ranged between 2% and 6%.

Other 2018 Changes

A significant increase in the standard deduction: the standard deduction nearly doubles, from $12,700 to $24,000 for married couples. Under pre-Act law, corporations are subject to progressive tax rates with the maximum rate of 35%. Under the new law, corporations are subject to a flat rate of 21%. Obamacare Individual Mandate is abolished. Under the new legislation, the deduction for all state and local taxes combined cannot exceed $10,000. These taxes include state and local income, sales, real estate, or property taxes. The Tax Cuts and Job acts keeps the AMT (Alternative Minimum Taxes) , but raises the exemption and phase out levels from 2018 through 2025. As a result, it will affect 200,000 tax filers instead of the 5 million affected in 2017.The Alternative Minimum Tax is a mandatory alternative to the standard income tax. It gets triggered when taxpayers make a certain income. It eliminates many deductions for those in higher brackets to make sure they pay at least some axes. The new 20% deduction of “Qualified†Business Income – a 20 percent deduction is available to entrepreneurs, subject to certain limits. You may get the break if your taxable income is below $157,500 if single, or $315,000 if married.

If you have any questions, don’t hesitate to contact us.

{kind=link}